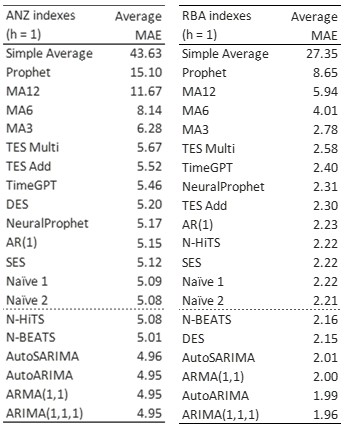

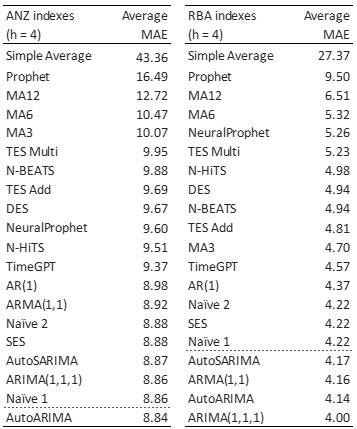

Forecast Accuracy of Statistical and Machine Learning Methods

This study compared the performance of traditional forecasting models and machine learning (ML) models on ANZ and RBA commodity price indices over one-month and four-month forecast horizons. The findings indicate that ARIMA variants consistently outperformed naïve benchmarks and delivered the best overall accuracy. In contrast, ML models struggled to consistently outperform the benchmarks, revealing no clear advantage. However, Prophet stood out as the worst-performing ML model, surpassing only the simple average, while NeuralProphet’s improved accuracy over Prophet was confirmed. A key observation was the substantial computational time required by ML models, which did not translate into better forecasting accuracy. These results suggest that analysts forecasting ANZ and RBA commodity prices should prioritize ARIMA models for their robustness and accuracy. For future research, in-depth optimization of ML models is recommended, particularly using Bayesian methods to automate hyperparameter tuning across models and indexes (AWS, 2025). These automated methods test various parameter combinations to identify the optimal settings which would give them a fairer representation in the study. Exploring longer forecast horizons could also yield valuable insights, as accurate long-term predictions are highly beneficial. Additionally, incorporating exogenous variables, such as macroeconomic indicators or weather data, may enhance predictive performance.

Average mean absolute error (MAE) of the models with forecast horizon (h) of 1 and 4 months.

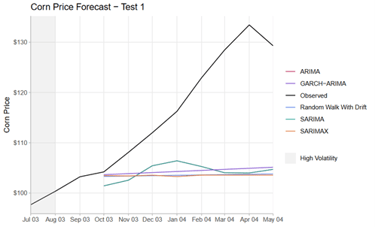

Forecasting Global Corn Price

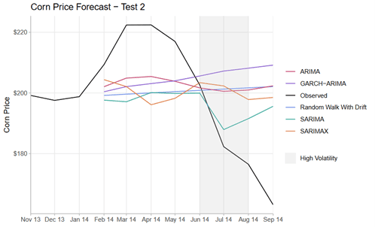

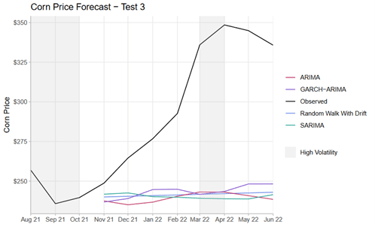

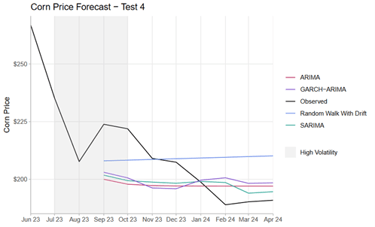

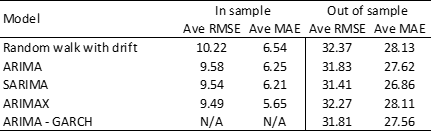

This project analyses how accurately global corn prices can be forecast eight months ahead using a range of time-series models. Using monthly data from 1993–2024, I compared a random walk benchmark against ARIMA, SARIMA, ARIMAX and ARIMA-GARCH models, evaluating performance across multiple rolling out-of-sample tests. The study incorporates production, demand, weather, geopolitical risk and input cost variables to assess whether fundamentals improve forecast accuracy, while also accounting for volatility clustering through GARCH. Results show that seasonal ARIMA models perform best on average, though all models struggle during sharp trend reversals, highlighting the limits of traditional econometric approaches for medium-term commodity price forecasting. The findings provide practical insights into price risk management for corn producers and consumers, and motivate further work using higher-frequency data and machine learning methods

Plots of the forecasting models at each test date.

Average error of the forecast models across the test dates.