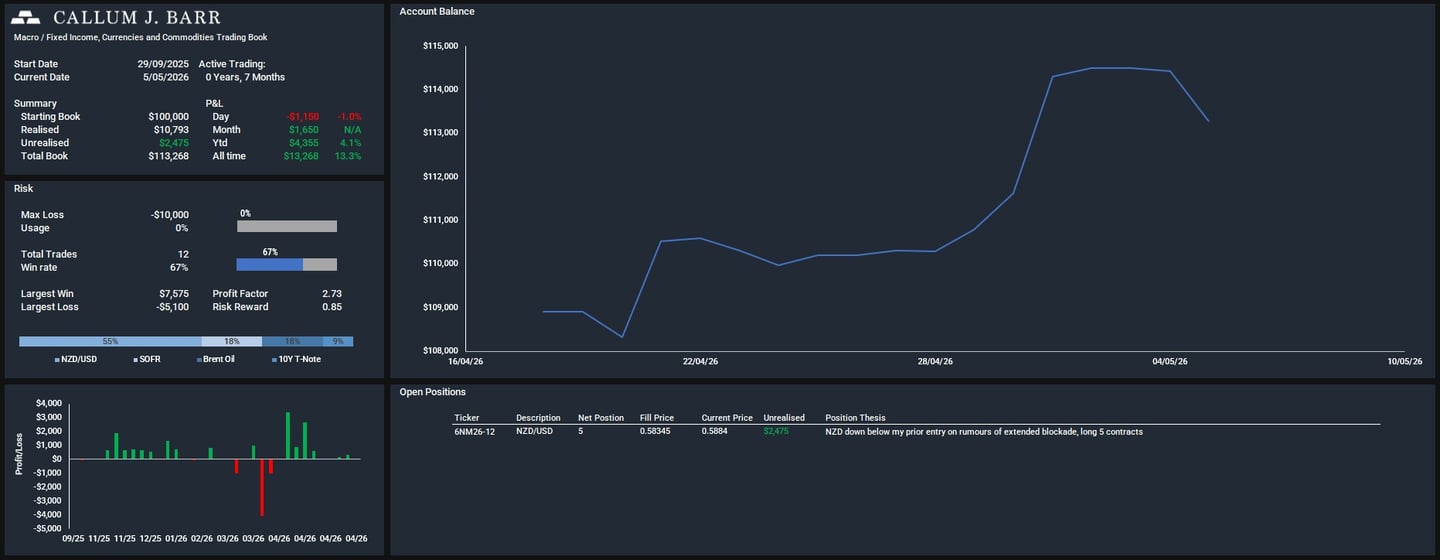

I enjoy following macroeconomic news and forming trading opinions based on it. To track how these ideas play out, I began paper trading futures on the CME Group’s platform. This allows me to apply the theory I learned while preparing for and passing the National Commodity Futures Exam (Series 3), as well as evaluate the performance of my economic views in real-world market conditions. The portfolio started with an $100,000 cash value.

Futures Trading

Trade 1:

Bought wrong contract (should have been 2026), therefore sold straight away for small loss of $25.

Trade 2:

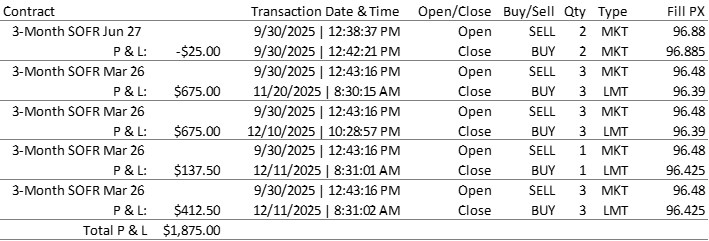

Instrument: SOFR 3-month Mar 26

Position: Short 10

Period: 30/9/25 – 11/12/25

Total P&L: $1,875

Thesis:

Market pricing aggressive Federal Reserve rate cuts despite CPI near 3%.

Inflation risks from tariffs remained due to tariff pause negotiation and importers stockpiling inventories prior to tariff start dates.

March contract was selected to allow flexibility around up incoming macro events and economic data releases.

Execution:

Closed out 3 contracts early to capture gains.

There was more uncertainty as the government shutdown.

Sold 3 contracts before Federal Reserve meeting to lock in more profits and held 4 through the meeting for upside potential.

Sold after meeting to close out position, unsure of next move and Fed was split on what to do next.

Trade 2: 3-month SOFR Mar 26 Trade log.

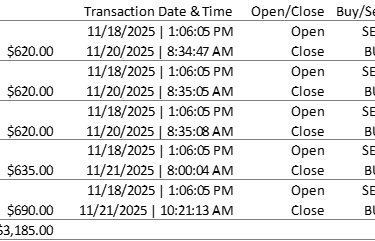

Trade 3:

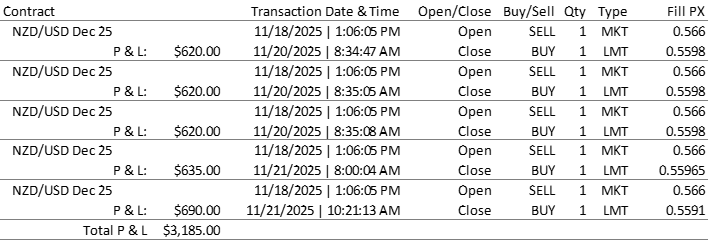

Instrument: NZD/USD Dec 25

Position: Short 5

Period: 18/11/2025 – 21/11/2025

Total P&L: $3,185

Thesis:

Economic conditions in New Zealand remained weak, suggesting further OCR cuts were likely

US monetary policy was expected to remain tighter relative to New Zealand, supporting USD strength versus NZD.

The trade expressed a view on widening interest rate differentials between the two economies.

Execution:

Entered a short NZD/USD position ahead of the OCR decision to position for continued NZD weakness.

Strong favorable price movement resulted in a sell limit order being triggered prior to the OCR announcement.

Trade 3: NZD/USD Trade log.

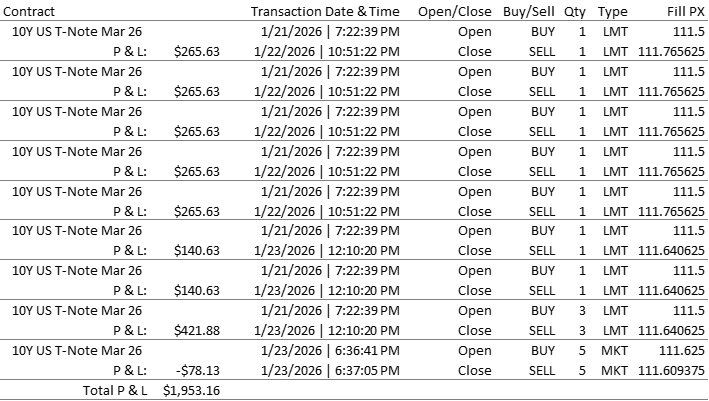

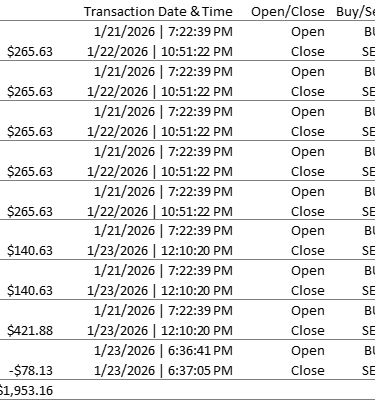

Trade 4:

Instrument: US 10Y T-Notes Mar 26

Position: Long 10

Period: 21/01/2026 – 23/01/2026

Total P&L: $2,031

Thesis:

Elevated geopolitical tension regarding military invasion of Greenland caused 10y T-Note yields to rise and prices to decrease.

Weaker US jobs data increased expectations of Federal Reserve Rate cuts.

Institutional support for Federal Reserve independence reduced the likelihood of sustained yield increases.

Execution:

Military invasion was ruled out over the next few days.

Five contracts were closed via a limit order as prices rebounded, securing early profits.

Remaining 5 contracts were closed manually once the original thesis had played out.

During position flattening, an execution error briefly resulted in an unintended long position, which was immediately closed for a small loss.

Trade 4: 10Y US T-Note trade log.

Trade 5:

Instrument: NZD/USD Jun 26

Position: Long 5

Period: 01/02/2026 – Present

Total P&L: Unrealised

Thesis:

NZ Inflation at upper end of RBNZ target range, from their perspective rate hikes expected in 2027. I think hike could occur in 2026.

In the US, labour market momentum appears to be slowing and tariff-driven inflation is increasingly viewed as transitory. The Fed’s reaction function appears biased toward holding or easing.

The trade expressed a view on narrowing NZ–US interest rate differential, driven by relatively tighter policy in New Zealand and looser policy in the United States.

Execution:

Entered a long NZD/USD position.

Intend to hold through several economic data events.

Liquidity is low which has caused short term volatility.

Closed position for modest gain following a more dovish than expected RBNZ (minimised inflation risks) and the outbreak of conflict involving US and Iran (USD typically strengthens in these conditions).

Trading Summary:

As of 26 January 2026, the portfolio is up $7,863 (7.8%) from an initial value of $100,000. Performance has been supported by partial profit-taking and positioning around key macro events. Losses to date have been driven by execution errors rather than thesis breakdown.